Cross Market Pricing Explained

Agiblocks now supports a user to (partially) price a contract across 2 futures markets trading in the same currency. This is common for pricing or to “lock in“ the “White Premium“ in the Sugar trade, but could also be used in other contracts where counterparties agree (partially) price or to lock in the arbitrage between two markets, or when companies to choose to (partially) hedge based on arbitrage between markets.

In Agiblocks, such a cross market pricing will be defined through a cross markets spread instrument. This cross market spread instrument enables a user to identify the (different) cross markets pricings.

Cross Market Pricing Requires Configuration

The implementation of Cross Market Pricing requires to define and configure cross markets instruments in Agiblocks.

Configuration must be executed by Agiboo to ensure that the functionality meets all customer requirements, as it has an impact throughout the Agiblocks system.

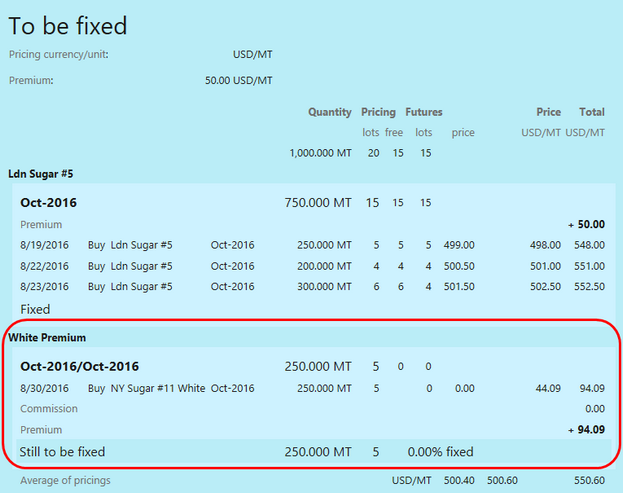

Cross Market Spread Master data (White Premium example)

A new Master data element labeled Cross market spreads is used to configure cross market pricing. This Master data item may only be created by an Agiboo consultant.

If cross market pricing has been configured, additional tabs will appear in the pricing edit box. The example below uses a White Premium configuration between Sugar #5 and NY Sugar #11. In it, Agiblocks shows the following tabs:

| 1. | Price: to price against Sugar #5 (the default pricing instrument) |

| 2. | Roll: to roll pricing periods within Sugar #5, either forward or backward |

| 3. | White Premium: to price the White Premium in order to roll the pricing instrument from Sugar #5 to NY Sugar #11. (The White Premium is fixed and will be added to the original premium.) |

| 4. | Price NY Sugar #11 White: it is also possible to fix the target rolling instrument first (e.g. NY Sugar #11 White); White Premium will then become to-be-fixed. |

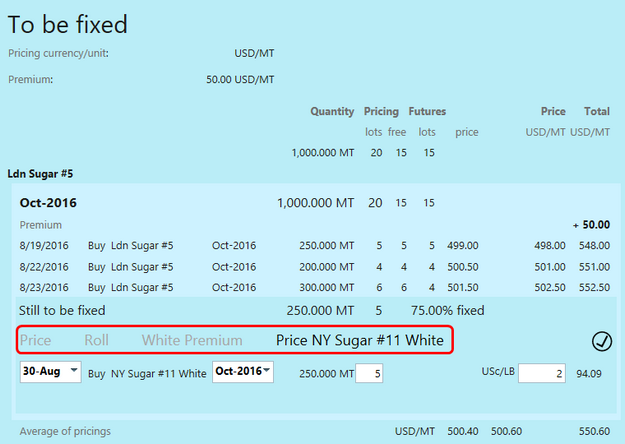

Effectively pricing the White Premium rolls the remaining pricing to NY Sugar #11 and vice-versa. pricing the NY Sugar #11 rolls the remaining pricing to White Premium.

When pricing a White Premium a user needs to enter:

- The trade date (by default today, though the system allows selecting a few days back)

- Which period in the NY Sugar #11 is used (by default the nearest period)

- How many lots are involved (by default all lots that are still to be fixed)

- The agreed White Premium price (no default value)

After applying the NY Sugar #11 pricing the screen will end up like this: